Battery-grade lithium carbonate prices, after staying flat for two weeks, posted a weekly gain of 0.83% during May 26 and June 2 to Yuan 305,000/tonne as of last Friday. The last material price hike was observed in late April when the prices surged Yuan 120,000/t to around Yuan 300,000/t. The prices of battery-grade lithium hydroxide, on the other hand, stood at Yuan 317,000/t, flat from a week earlier.

Figure 1-1. Lithium carbonate and hydroxide price trend (Yuan/tonne)

Source: Mysteel

As lithium compound prices struggle for a direction, both upstream and downstream players eye the end demand as a key indication to the follow-up price trend. To be specific, only a bottoming-out end market will encourage the downstream players with low in-plant stocks to fill up their warehouses; otherwise, the demand recovery will be short lived which is unable to boost the market transactions.

With this in mind, Mysteel has done a thorough research of the lithium battery market to try to give some clues concerning the market dynamics. More details could be found from Mysteel monthly output and production scheduling survey released on the 8th of the month.

In terms of new energy vehicle (NEV) sales, BYD sold a total of 239,000 passenger vehicles in May, up 109% y/y due to a low base last year when the COVID-19 pandemic ravaged and up 14% m/m, indicating an improving NEV market. It is estimated that the overall NEV sales in China could grow 12% m/m to 680,000 units in May based on public data.

Table 1-1. Mainstream NEV brands' sales and estimated total sales (10,000 units)

Sources: Relative official websites, Mysteel

In the energy storage battery end, the newly installed capacity amounted to 2.9 GW in the first quarter, and the capacity planning is also ten times the scale last year with rapid advancing, according to Mysteel. Meanwhile, the feedback from battery material and battery cell factories is also solid evidence that the momentum of energy storage battery has been far larger than that of the power battery.

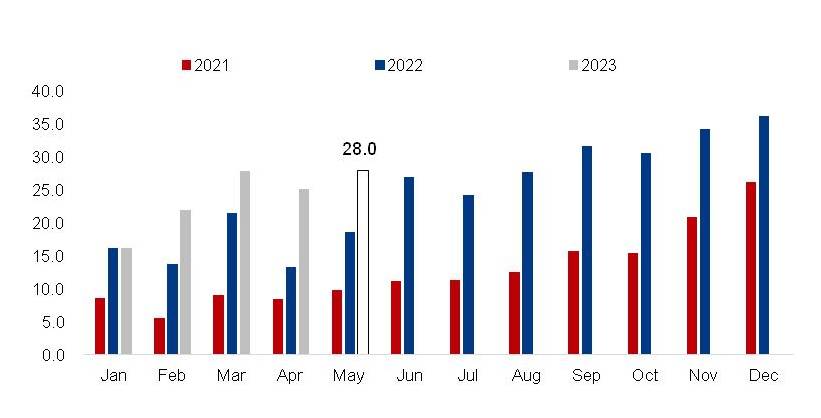

BYD's combined installed capacity of power and energy storage battery was 11.49 GWh in May, a 15.5% increase compared with 9.95 GWh in April. Generally speaking, the demand growth of LFP battery outperformed that of ternary battery thanks to the thriving energy storage market, while the installed capacity of power battery still took the lion's share of 28 GWh out of the estimated 30 GWh in May, up 12% m/m.

Figure 1-2. Power battery installed capacity (GWh)

Source: Mysteel

On the raw material end, the output of LFP and ternary cathode material is estimated to jump 39.7% and 9.5% m/m respectively to 130,000 t and 46,000 t in May, and together they would consume 37,000-39,000 t of lithium carbonate (considering mainly 6-series cathode material). Since the production of LFP and ternary cathode material is projected to keep rising in June, some manufacturers have ramped up their inquiries for raw materials, but are still sensitive towards lithium compound prices.

The upstream lithium carbonate manufacturers have been destocking when the prices rebounded earlier in order to seize the upper hand in pricing in the second half of 2023. Most manufacturers are likely to keep their stocks at a low level of roughly 40,000 t, and the monthly output is expected at 32,000-33,000 t should lithium carbonate prices hover around Yuan 300,000/t, based on the successful big deals at the market.

Taken together, lithium carbonate prices' moving range will move up on recovering demand but is expected to stop at around Yuan 350,000/t in light of the wrestling between upstream and downstream players.

The upstream players now count on the downstream manufacturers' compulsory stockpiling once the end demand rebounds rapidly as the seasonal high is on the way. At present, the downstream manufacturers' lithium carbonate stocks could sustain their production for merely half a month, and their warehouses are far from fulfilled. Therefore, the upstream will not compromise easily on lithium carbonate prices.

However, the downstream plays, namely the battery cell manufacturers, are still with abundant finished battery cell stocks, which would play as a bargaining chip against the upstream if the end demand does pick up.

Figure 1-3. Battery cell manufacturers' stocks are on the rise (GWh)

Source: Mysteel

The game between upstream and downstream players centering lithium carbonate prices is far from a close. Mysteel believes that lithium carbonate prices will move between Yuan 320,000-350,000/t after taking into account the recovering NEV market and thriving energy storage demand as well as battery manufacturers' stockpiling plans.

Written by Aggie Hu, huchenying@mysteel.com