It is expected that China's lithium carbonate spot prices will finally regain momentum on the unexpected maintenance of two major producers in China, against the traditional seasonal high in September and October, per Mysteel analysis.

Source: GFEX

Yesterday September 11, the most-traded GFEX LC closed the day session with a drastic intraday rise of 7.91%, boosted by the rumor that CATL was mulling over the production suspension of its lithium projects in Jiangxi Province for maintenance, which went viral on the morning.

Later in the same day, UBS, a Swiss banking giant, said it its newly released research report that "CATL decided to suspend its lepidolite operations in Jiangxi at a meeting held on September 10". Should CATL's lithium projects come to a full suspension as the rumor said, China's monthly lithium carbonate production could be reduced by as much as 8%.

Furthermore, Jiangxi Jiuling, a leading lithium chemicals producer in China, released a notice post the GFEX day session that the company plans to suspend the production of Jiangxi Chunyou Lithium (mine) and Yifeng Jiuyu Lithium (separation plant) over September 12-27 for maintenance.

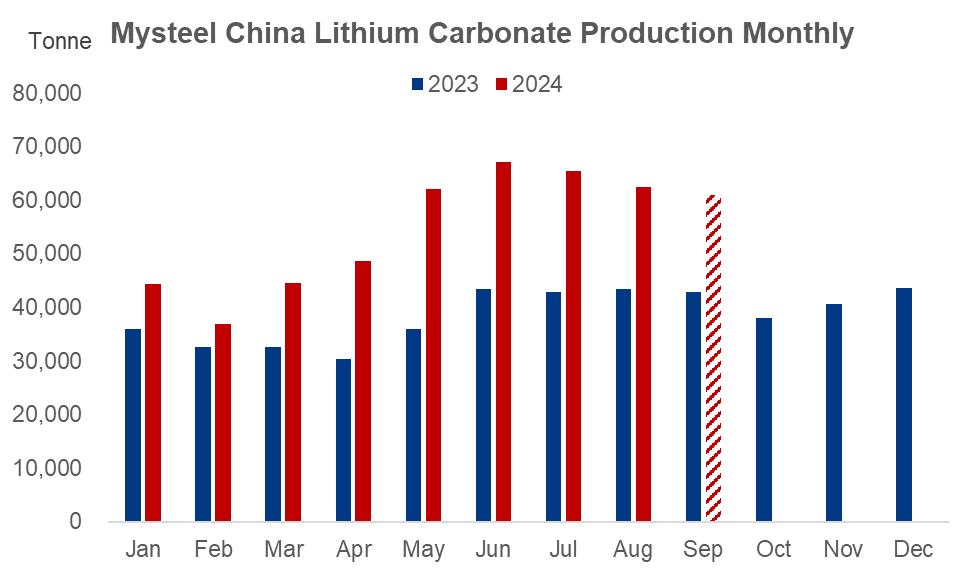

According to Mysteel survey, China's lithium carbonate production is estimated at 61,000 tonnes in September, down 2.18% from August primarily due to maintenance of several producers in Jiangxi and fewer tolling orders received amidst rapidly falling lithium carbonate prices.

Specially, CATL's unexpected maintenance will probably reduce the monthly production by 2,000 tonnes in September should it start from next week.

Source: Mysteel

Meanwhile, China's lithium carbonate imports are likely to remain low in September, after Chile lithium carbonate exports to China showed a monthly fall of 22.9% in August on the anticipation that the lithium carbonate supply in Argentina will stay flat until November.

On the demand side, China's LFP production is estimated at 234,600 tonnes in September according to Mysteel survey of 39 sampled producers, up 9.22% month on month. And the growth is likely to come from both the power battery and energy storage sectors.

Though China's ternary cathode materials production is projected to edge down 1.05% MoM at 57,700 tonnes in September based on 32 sampled producers, the monthly consumption of lithium carbonate is likely to amount to 81,000 tonnes after counting in the consumption in the LCO, LMO, LiPF6, and other traditional fields.

Taken together, China's lithium carbonate market is more than likely to see a supply deficit in September, which is likely to extend into October should the maintenance prolong.

Meanwhile, the spot prices will gain momentum with downstream players beginning to build stocks ahead of the National Day holiday.

Written by Aggie Hu, huchenying@mysteel.com