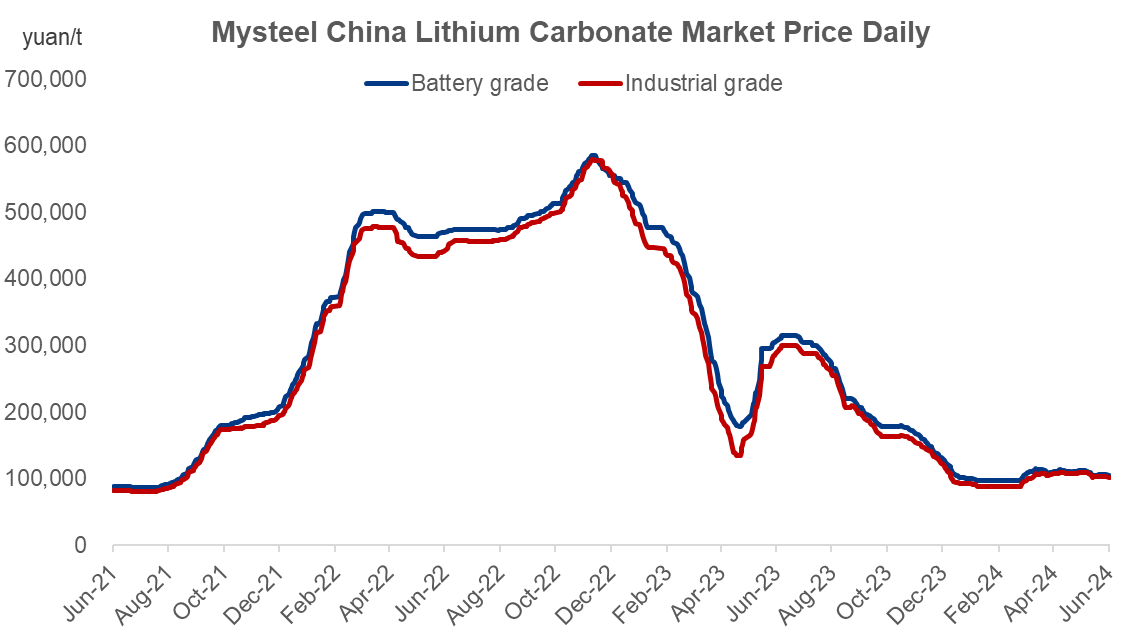

Lithium prices have been staying low since entering 2024 primarily due to slowing end-market demand, and a lingering supply surplus. However, the cost will probably rise with the lithium mines gradually going underground.

Source: Mysteel

On the demand side, global electric vehicle (EV) sales seem to be losing momentum in the face of reducing subsidies in both China and abroad. The global EVs sales growth is estimated at 20% in 2024, against 29% in 2023, data showed.

Many European countries have announced the tightening of subsidy policies for EVs. Among them, Germany, France, and the Netherlands are relatively more aggressive.

Germany announced on December 18, 2023 that it would no longer accept applications for EV purchase subsidies, following the United Kingdom (cancelled in June 2022).

In the Netherlands, only about 5% of existing passenger cars are fully electric. The government hopes to use subsidies to promote the use of EVs. People who buy or lease EVs in the Netherlands can receive subsidies, which, however, is down 12 million euros from 2023 and totals 87 million euros in 2024.

In France, it still retains the subsidies for EVs, and BEVs and FCVs with a price below 47,000 euros are eligible for subsidies of up to 7,000 euros. However, it is accompanied by a list of EV models that enjoy policy subsidies. And it seems that the EVs produced in China have been excluded from the list.

China ended the subsidies for EVs ended at the end of 2022, except for purchase tax exemptions and trade-in subsidies.

On the supply side, drastically rising lithium prices by 2022 attracted many investors and led to rapid capacity expansion. The market was therefore oversupplied with the rapid commissioning of overseas lithium projects and ending subsidies in China by the end of 2022.

It is expected that the global lithium market will remain oversupplied over 2024-2026 as more lithium projects are expected to come on stream, while the EVs sales growth is poised to slow down as mentioned in the previous session.

Apart from the fundamentals, the lithium market faces challenges from other aspects.

First, the cost of lithium carbonate is projected to rise as the lithium ore grade is declining.

Generally, the mining companies will give priority to the highest quality and most developed resources, and the marginal ore grade will decrease in the long run, corresponding to the increase in the average mining cost.

For example, Australia's mines basically adopt open-pit mining, but Greenbush and Cattlin are already working on underground mining research plans. Mt Finiss's second tenement BP33 will be underground; Wodgina's fourth phase is expected to be underground as well (put into production in 2026); and Mt Marion will begin underground mining in 2025.

In this case, the mining companies have explored multiple ways to control the cost, including laying off, selling assets, curtailing the production, M&A, and changing to new selling strategies.

Second, the competition over resources has been intensifying.

Taking CATL as an example, the company invested in Tianyi Lithium and holds 25% of the shares in the lithium carbonate smelting business. Besides, it also strategically invested in Zhicun Lithium and holds 23.2% of the shares. Overseas, CATL invested in Pilbara and holds 7.5% of the shares, and it also owns its own lithium mine in Jiangxi Province.

On the other hand, the mining companies are going downstream. For example, Tianqi Lithium Energy Australia delivered part of its spodumene concentrate to its Kwinana and Kemerton refineries. MRL holds 50% of Mt Marion and 50% of Wodgina's shrae (after the completion of the non-binding agreement), and plans to build its own lithium hydroxide refinery in Australia in the next 2-5 years. Other miners like Pilbara, Allkem, AMG, Core Lithium also have plans for lithium salt plants.

Lastly, the policy front has been re-shaping the lithium market constantly.

In November 2023, Zimbabwe's Finance Minister Mthuli Ncube said that lithium miners investing in the country have been asked to submit plans for local production of battery-grade lithium carbonate by March 2024. The Chilean tax bureau suddenly expanded the scope of the country's mining tax, and conducted a new round of tax assessment and re-taxed the lithium mining industry. In April 2024, the Santiago Court in Chile re-ruled the mining tax for 2017-2018, revoking the ruling conclusion of the Chilean government in 2022 that supported SQM's failure to pay mining taxes. In addition, the list of EV models announced by France that can receive government subsidies excludes EVs produced in China. The United States' IRA bill also targets to ban made-in-China EVs.

Taken together, the lithium market players shall stay alert to factors influencing the lithium prices and preserve their competitiveness to face the challenges lying ahead.

Written by Aggie Hu, huchenying@mysteel.com