I. Overview

China's power batter production growth slowed in July as most manufacturers had already finished stockpiling around mid-June. Lithium carbonate prices fluctuated following the demand side dynamics, which subsequently influenced the power battery production scheduling.

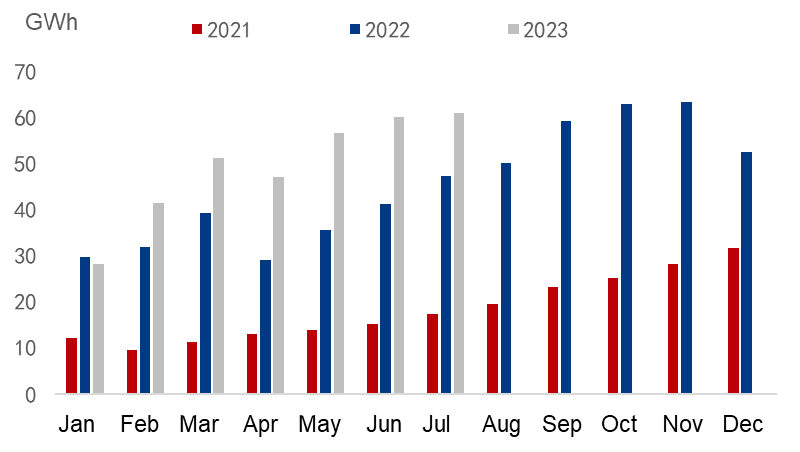

The production of power batteries recorded 61 GWh in July, a mild increase of 1.5% compared with June, and up 47.7% year on year (YoY), according to Mysteel survey. The year-to-date (YTD) production totaled 345.5 GWh, rising 36.1% YoY.

Specifically, the production of LFP power batteries dropped 4% MoM at 40.5 GWh in July, rising 32.4% compared with last year. The ternary power batteries production stood at 20.4 GWh, indicating a monthly growth of 15.3% and an annual jump of 22.9%.

Figure 1-1. China Power Battery Production

Sources: China Automotive Power Battery Industry Innovation Alliance (Power Battery Alliance), Mysteel

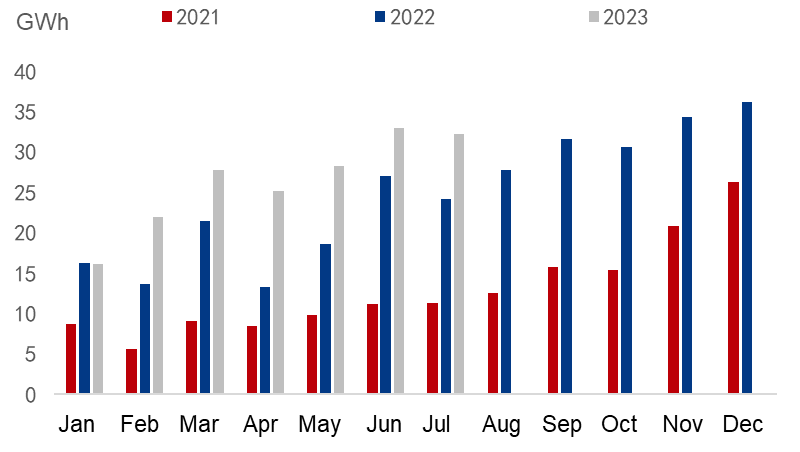

The total installed capacity of LFP and ternary power batteries was 21.7 GWh and 10.6 GWh respectively in July, down 4.4% and up 5% MoM respectively, with the total capacity falling 2.1% from June at 32.2 GWh.

Figure 1-2. China Power Battery Installed Capacity

Sources: Power Battery Alliance, Mysteel

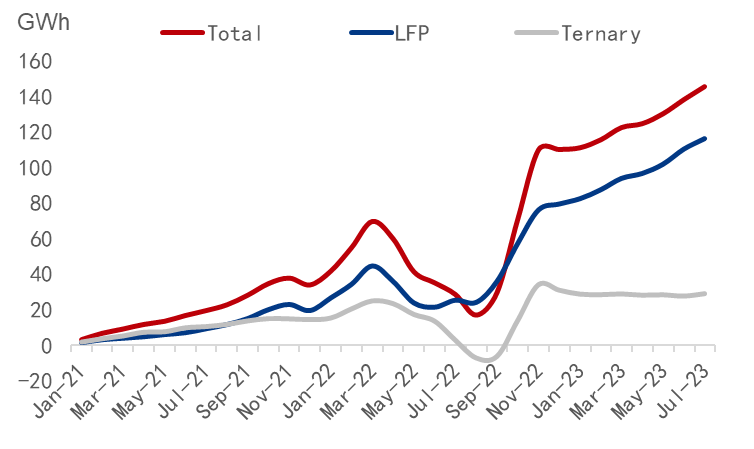

The cumulative power battery inventory climbed 5.3% MoM at 145.3 GWh in July, comprising of 116.2 GWh LFP power batteries and 28.8 GWh ternary power batteries, which added 5.3% and 4.9% MoM respectively, and equaled to three months and one month of July sales respectively.

Figure 1-3. Power Battery Manufacturers' In-plant Inventory

Sources: Power Battery Alliance, Mysteel

II. Power battery market breakdown by battery type and manufacturer

By battery type

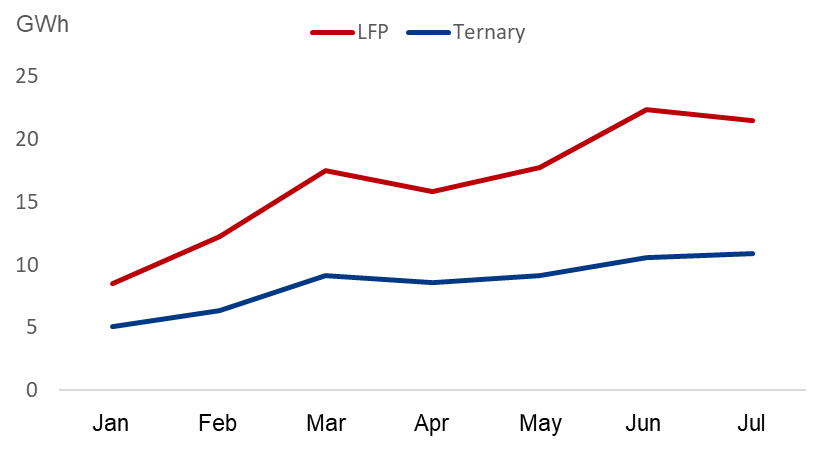

The installed capacity of LFP power batteries fell 3.8% from June at 21.5 GWh in July among new energy vehicles actually insured, with ternary power batteries recording a monthly increase of 2.5% at 10.9 GWh. LFP power batteries still took more than two thirds of the entire market despite a monthly decrease.

Figure 1-4. LFP and Ternary Power Batteries Installed Capacity

Source: Mysteel

By battery type and vehicle model

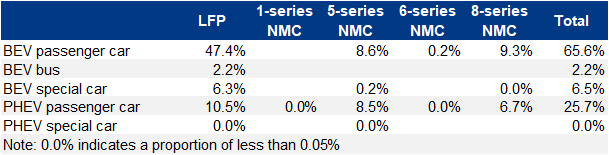

LFP power batteries were mostly installed to battery electric passenger vehicles, with a total installed capacity of 15.4 GWh, taking up 47.4% of the combined installed capacity of power batteries. For ternary power batteries, 5 and 8-series NMC power batteries were relatively more popular and were mostly applied to plug-in hybrid electric passenger vehicles and battery electric passenger vehicles.

Figure 1-1. LFP and Ternary Power Batteries Installed Capacity by Vehicle Model

Source: Mysteel

In addition, the total power battery installed capacity falling 2.1% MoM in July was mainly attributed to falling LFP power battery capacity installed to battery electric passenger vehicles.

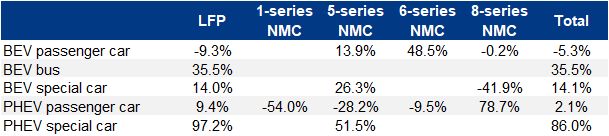

Table 1-2. Monthly Growth of LFP and Ternary Power Batteries Installed Capacity by Vehicle Model

Source: Mysteel

By general power battery manufacturer

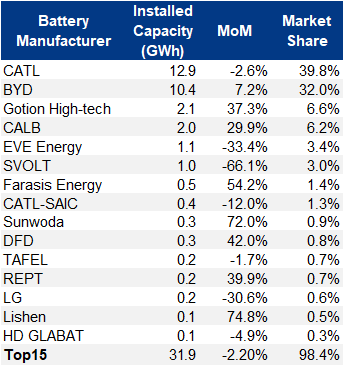

The top 15 power battery manufacturers by installed capacity had 31.9 GWh of power batteries installed in July, down slightly 2.2% MoM. Apart from CATL and BYD who performed steadily, Gotion High-tech and CALB Tech both demonstrated quick MoM growth.

Table 1-3. Power Battery Installed Capacity by Manufacturer

Source: Mysteel

In the below sections analyzing the battery type-wise installed capacity of individual manufacturers, Mysteel will look at both the monthly and bi-monthly growth as the former is easily affected by a low or high base in the previous month.

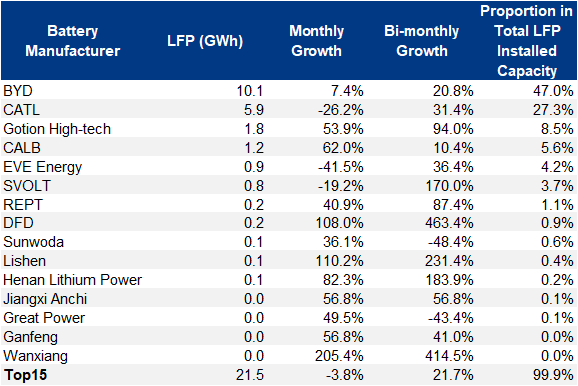

By LFP power battery manufacturer

The installed capacity of LFP power batteries lost 3.8% MoM in July mainly due to falling installation of CATL batteries. In detail, CATL's installed LFP power battery capacity fell 26.2% compared with June at 5.9 GWh in July but rose 31.4% on a bi-monthly basis. BYD still championed with a monthly increase of 7.4% and a bi-monthly jumped of 20.8%. Gotion High-tech, REPT, and DFD all demonstrated momentum on a monthly and bi-monthly basis.

Table 1-4. LFP Power Battery Installed Capacity by Manufacturer

Source: Mysteel

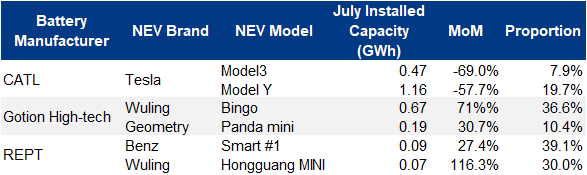

The performance of battery manufacturers is closely related to the sales situation of its clients. For example, CATL's monthly fall in LFP power battery installed capacity in July was primarily attributed to Tesla's focusing on export businesses in July, reducing the capacity of batteries installed to vehicles sold domestically.

Contrarily, the outstanding performance of Gotion High-tech and REPT was owing to the popularity of Wuling Bingo EV and Wuling Hongguang Mini EV respectively.

Table 1-5. Selected LFP Battery Manufacturers and Their Clients' Power Battery Installed Capacity

Source: Mysteel

By ternary power battery manufacturer

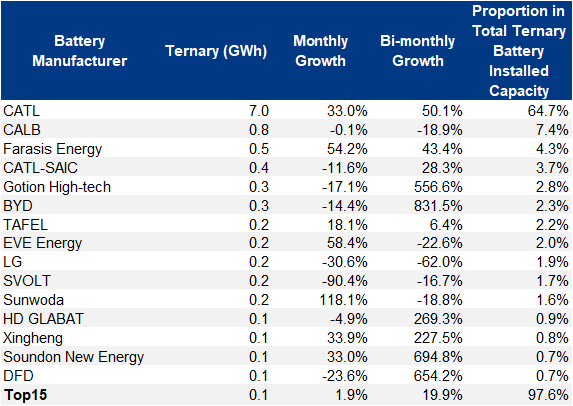

CATL was still the absolute leader in the ternary power battery sector, taking up 64.7% of the total market.

Table 1-6. Ternary Power Battery Installed Capacity by Manufacturer

Source: Mysteel

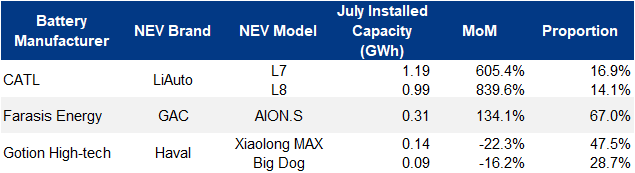

Among them, some brands stood out in terms of monthly increase thanks to the emergence of hot-selling vehicle models and engagement of new clients. For example, LiAuto changed its supplier from SVOLT to CATL in July, contributing to the palpable MoM growth of CATL by installed capacity in the month.

For Gotion High-tech, the fall in installed capacity was because Haval Xiaolong Max and Haval Big Dog weakened by sales volume.

Table 1-7. Selected Ternary Battery Manufacturers and Their Clients' Power Battery Installed Capacity

Source: Mysteel

Summary

The inventory of power batteries rose in July as a result of falling installed capacity, despite slowing production following the end of intensive stockpiling among battery manufacturers.

In August, the battery manufacturers focused on de-stocking, and purchased lithium carbonate on rigid demand.

According to Mysteel survey, both upstream salt smelters and downstream battery manufacturers kept their lithium carbonate inventory at a low level. When lithium carbonate prices have dropped below the breakeven point of smelters who relied on outsourced lithium ore, the prices are expected to bottom out once the demand picks up.

On the demand side, falling deposit interest rates are projected to stimulus the consumer market, including new energy vehicle consumption, which is expected to be verified by end-September. Therefore, Mysteel is relatively optimistic over the NEV and battery sales in the fourth quarter.

Written by Aggie Hu, huchenying@mysteel.com