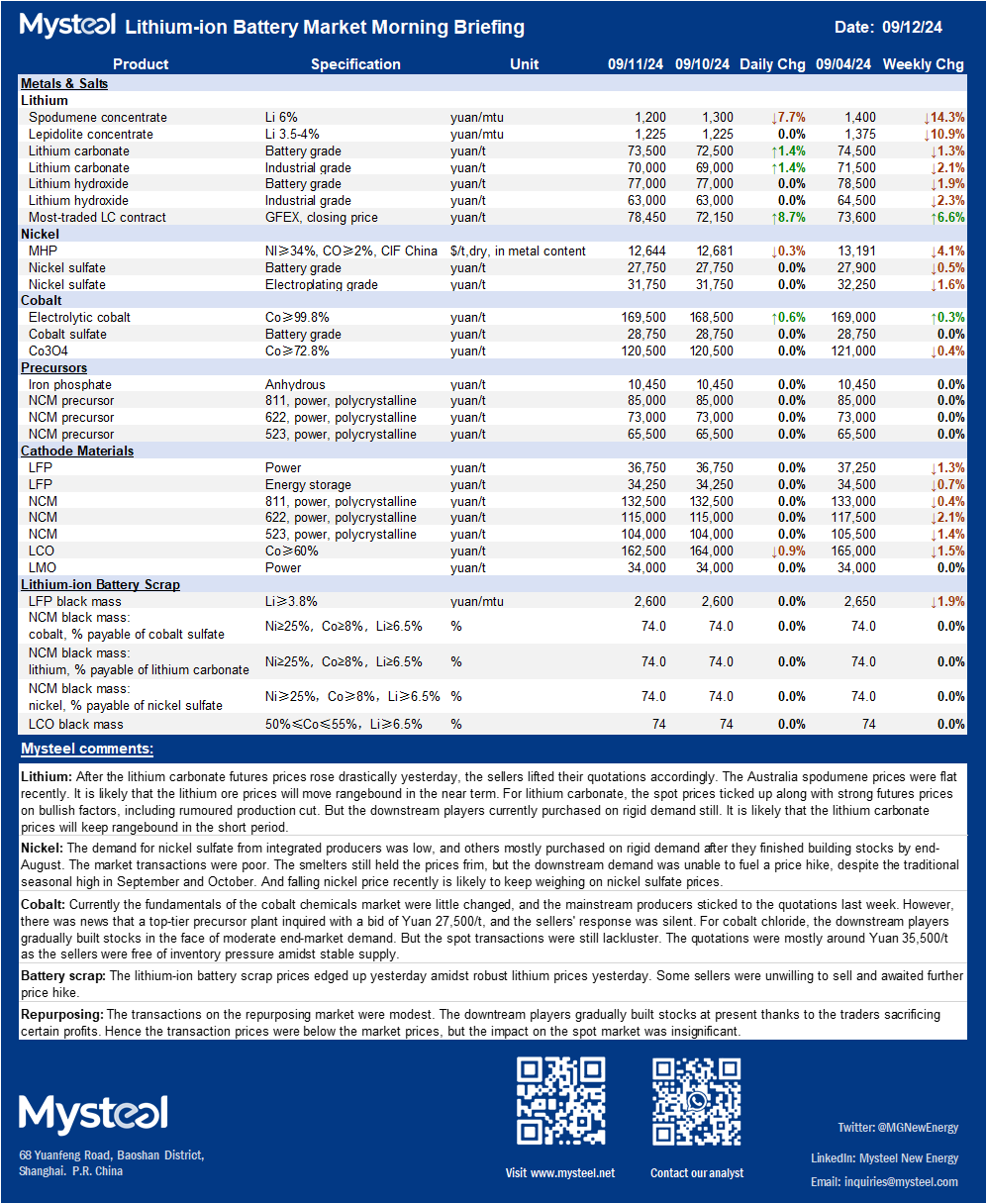

Lithium: After the lithium carbonate futures prices rose drastically yesterday, the sellers lifted their quotations accordingly. The Australia spodumene prices were flat recently. It is likely that the lithium ore prices will move rangebound in the near term. For lithium carbonate, the spot prices ticked up along with strong futures prices on bullish factors, including rumoured production cut. But the downstream players currently purchased on rigid demand still. It is likely that the lithium carbonate prices will keep rangebound in the short period.

Nickel: The demand for nickel sulfate from integrated producers was low, and others mostly purchased on rigid demand after they finished building stocks by end-August. The market transactions were poor. The smelters still held the prices frim, but the downstream demand was unable to fuel a price hike, despite the traditional seasonal high in September and October. And falling nickel price recently is likely to keep weighing on nickel sulfate prices.

Cobalt: Currently the fundamentals of the cobalt chemicals market were little changed, and the mainstream producers sticked to the quotations last week. However, there was news that a top-tier precursor plant inquired with a bid of Yuan 27,500/t, and the sellers' response was silent. For cobalt chloride, the downstream players gradually built stocks in the face of moderate end-market demand. But the spot transactions were still lackluster. The quotations were mostly around Yuan 35,500/t as the sellers were free of inventory pressure amidst stable supply.

Battery scrap: The lithium-ion battery scrap prices edged up yesterday amidst robust lithium prices yesterday. Some sellers were unwilling to sell and awaited further price hike.

Repurposing: The transactions on the repurposing market were modest. The downtream players gradually built stocks at present thanks to the traders sacrificing certain profits. Hence the transaction prices were below the market prices, but the impact on the spot market was insignificant.