Key Highlights:

- In July 2024, the Third Plenary Session of the 20th CPC Central Committee called for the advancement of shifting consumption tax collection further downstream and steadily transferring the tax revenue to local governments. GL Consulting's speculations about key reforms regarding the consumption tax on refined oil products include: 1) The collection of the consumption tax will move from the production stage at refineries to the point of sale at petrol stations. 2) Consumption tax revenues will be steadily transferred to local governments to achieve tax-sharing mechanism between central and local governments. The incremental portion of these revenues may be fully allocated to local governments, while the allocation of the base portion remains undecided; 3) The fixed consumption tax rates will remain unchanged, with gasoline at CNY 1.52/liter (CNY 2,109.8/tonne), diesel at CNY 1.2/liter (CNY 1,411.2/tonne), and aviation kerosene at CNY 1.2/liter (currently exempt from consumption tax).

- Impacts on the refined oil product market: 1) Production segment: Inefficient production capacities that primarily rely on tax evasion for profits will be phased out at a faster pace, state-owned enterprises (SOEs) will gain more market shares, and the price gap between state-owned and independent refineries will narrow. 2) Circulation segment: Opportunities for tax evasion through blending components will disappear, leading to more compliant operations and a higher tax levy ratio. This will further boost market share concentration in the domestic refined oil product market. 3) Retail segment: Significant reductions in price discounts will undermine the competitiveness of private petrol stations. Stricter local regulations and the increased adoption of electric vehicles (EVs) will further challenge the survival of these stations, likely leading to a substantial decrease in their numbers and an increase in the market share of SOEs.

Background: Conditions Are Mature for A Tax Levy Shift

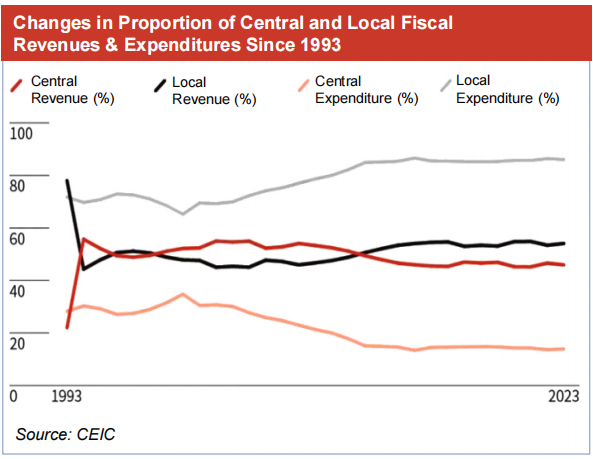

Currently, consumption tax in China is centrally collected, with all tax revenues going to the central government. The consumption tax on gasoline and diesel is levied at refineries mainly due to regulatory and collection convenience. Additionally, the previous large number of petrol stations made it impractical to regulate the entire supply chain effectively if the tax were collected at the point of sale.

Economic downturn pressures, along with tax cuts and fee reductions, have increased fiscal pressure on local governments, underscoring the necessity for fiscal and tax system reforms. Since 2019, the gradual expansion of the tax control system at petrol stations from pilot areas to nationwide application, along with the anticipated full launch of the Golden Tax System (GTS) Phase IV in 2024, indicates that conditions for the tax levy shift will be mature once the detailed rules for tax-sharing between central and local governments are clarified.

Challenges to Independent Refineries' Survival

To increase price competitiveness, independent refineries previously avoided taxes by not issuing invoices or using chemical product invoices, which are not subject to consumption tax, for gasoline and gasoil sales. Moving the consumption tax downstream will completely end these non-compliant operations, leading to rational wholesale prices and a narrowed retail-wholesale price gap. This will significantly reduce profits for private petrol stations that primarily rely on low-cost resources, and traders who benefitted from tax evasion.

Meanwhile, shifting the collection point of consumption tax downstream necessitates a tax-sharing mechanism between central and local governments, which will stimulate local regulatory enthusiasm. This change will inevitably result in stricter measures against tax evasion in petrol stations' procurement and sales processes. Consequently, private petrol stations are likely to offer fewer discounts, diminishing their competitive edge relative to state-owned counterparts.

EVs are increasingly appealing to price-sensitive consumers, who constitute the core customer base of private petrol stations. This trend, combined with declining sales and profits, intensifies competitive pressures on these stations, signaling a likely period of industry consolidation and a significant reduction in the number of private petrol stations.

Major state-owned refineries will face higher external procurement costs. However, their integrated refining and petrochemical operations, along with comprehensive upstream and downstream support, will enable them to maintain their competitive advantage and potentially expand their market shares in both the wholesale and retail sectors. This will lead to higher market concentration within the refined oil product market.

Possible Decline in Tax Revenues for Major Producers; Gains for Non-Refining Provinces

Currently, local governments collect VAT, urban maintenance and construction tax, and educational surcharges based on the consumption tax levied at refineries. It is still uncertain whether local governments will receive more tax revenues if the incremental portion of consumption tax revenues from refined oil products are shared between central and local government. The financial impact will remain unclear until detailed rules are published. GL Consulting speculates that the consumption tax revenues will be steadily transferred to localities to achieve tax-sharing between central and local governments, and the incremental portion of these revenues may be fully allocated to local governments.

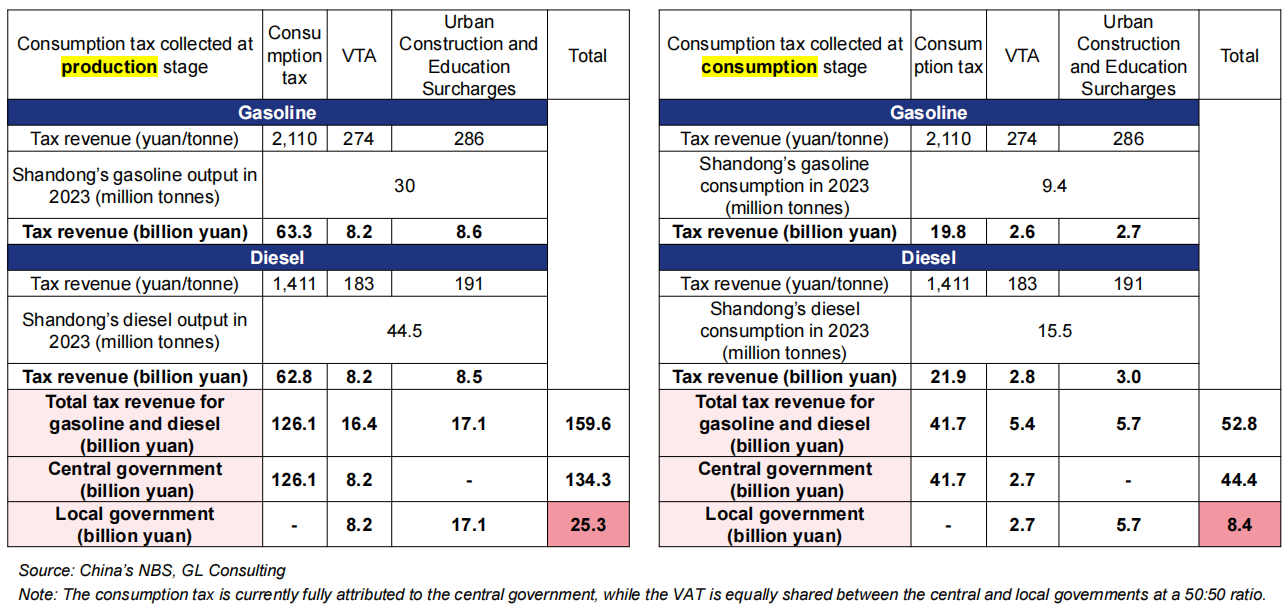

Using Shandong, which boasts the most concentrated refining capacity of independent refineries, as an example, we examine the differences in consumption tax revenues derived from production versus consumption segments. In 2023, Shandong's nominal production of gasoline and diesel (sold invoiced as gasoline and diesel) was 30 million tonnes and 44.5 million tonnes, respectively. When the consumption tax on refined oil products is collected at the point of production, Shandong can obtain a total of 25.3 billion yuan in VAT, urban maintenance and construction tax, and educational surcharges.

Shandong's gasoline and diesel consumption in 2023 reached 9.4 million tonnes and 15.5 million tonnes, respectively. If the tax levy shifts to the point of sale, the tax revenue will drop to 8.4 billion yuan, a decrease of 16.9 billion yuan compared to collecting the tax at refineries. This represents 41% of Shandong's total refined oil product consumption tax revenue of 41.7 billion yuan. Therefore, the region would need 41% of the consumption tax distribution to maintain current revenue levels. However, declining gasoline and diesel consumption due to the increasing adoption of EVs and industrial restructuring may still result in reduced tax revenues.

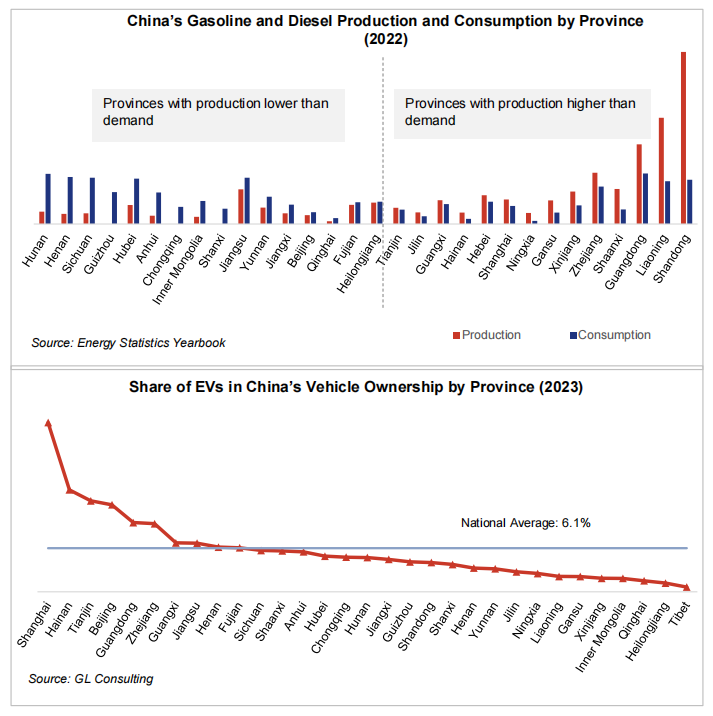

In contrast, regions like Shanxi, Chongqing, and Guizhou, which lack refineries and have historically missed out on consumption tax-derived revenues (i.e. tax imposed on top of the consumption tax), will benefit from increased tax revenue with this reform.

To get detailed full text, send an email to glconsulting@mysteel.com

Edited by Jade Yu, yujiajun@mysteel.com