The intensive issuance of hydrogen energy policies in China has spurred active involvement from enterprises in hydrogen projects. In terms of hydrogen production, the number of green hydrogen projects surged in Q1 2024, surpassing 80% of the total for 2023, with planned investments exceeding those of 2023.

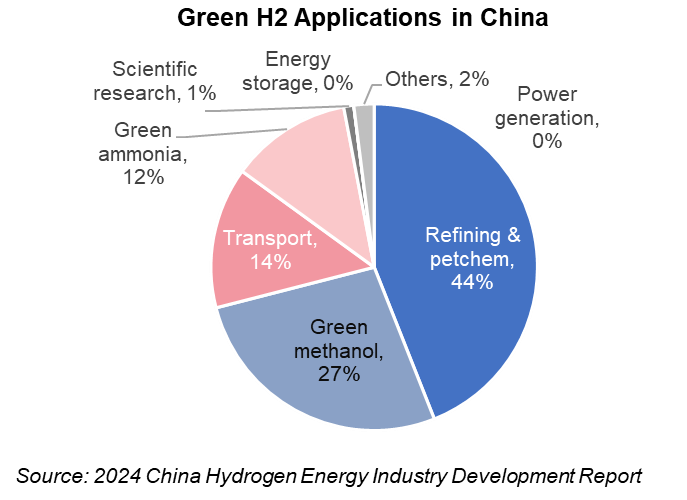

On the application sector, the chemical industry is the primary consumer of domestic green hydrogen, especially for ammonia and methanol production. The EU's Carbon Border Adjustment Mechanism (CBAM) has driven demand for green methanol, making it the preferred choice for shipping decarbonization. Therefore, from the second half of 2023, new projects are shifting focus from green ammonia to green methanol.

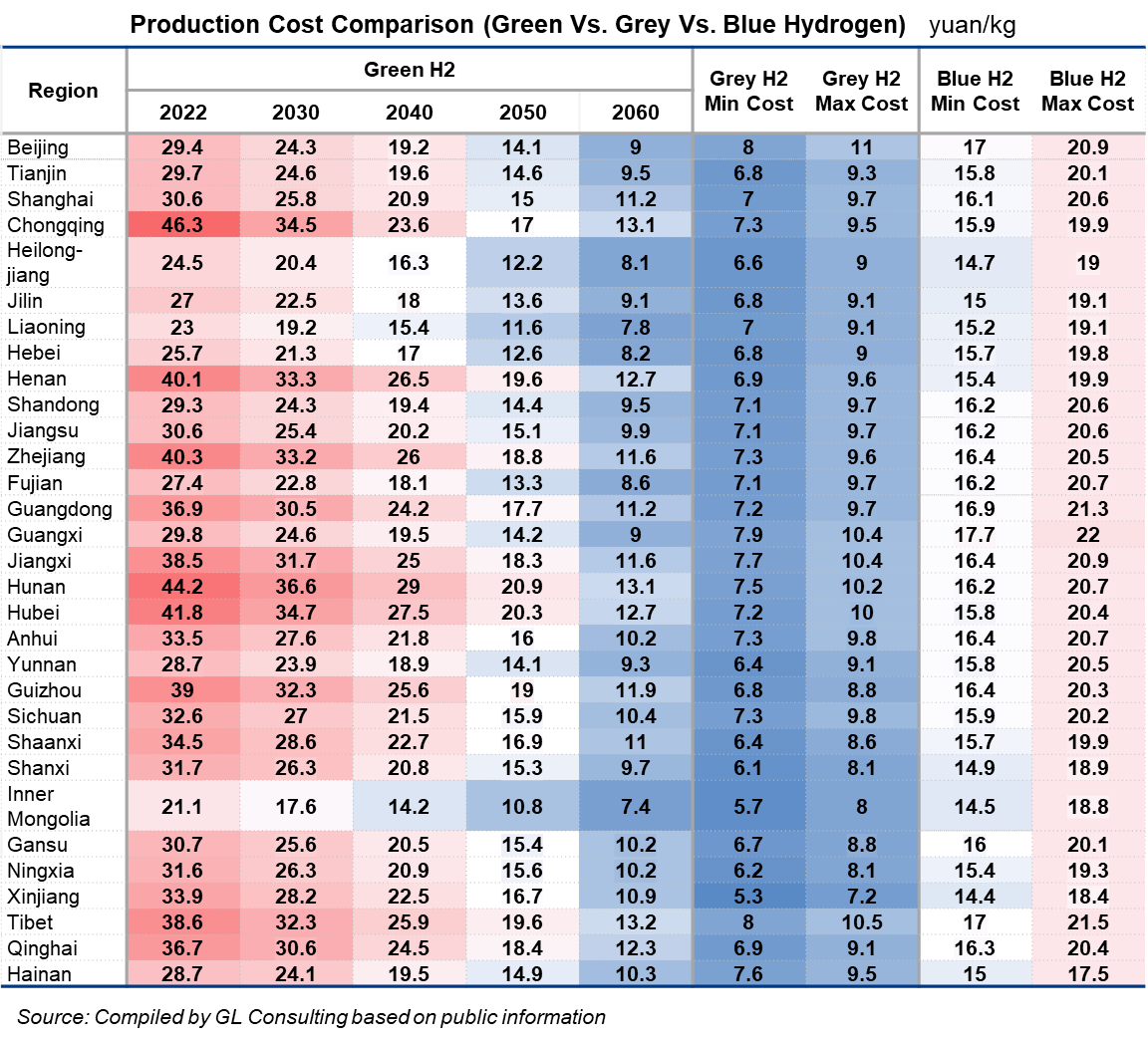

However, higher costs of green hydrogen compared to grey hydrogen and the lack of refined carbon emission trading policies present medium to long-term challenges. Only nine provinces with abundant renewable energy such as wind and solar resources are expected to achieve cost parity between green and grey hydrogen by 2060.

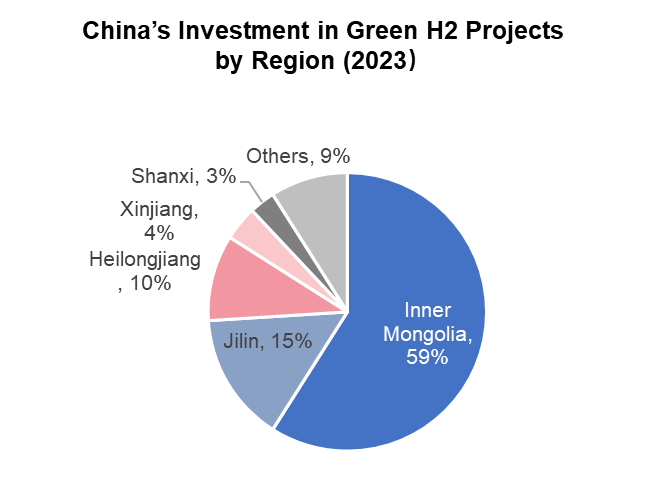

Inner Mongolia Leads with 59% of China's Hydrogen Project Investment

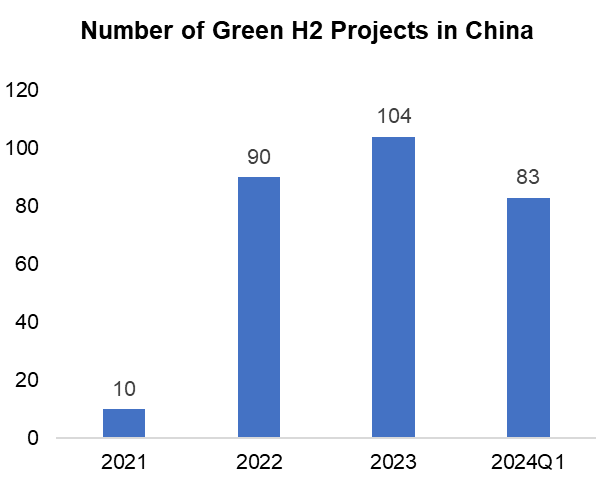

Policy support and technological advancements have accelerated green hydrogen projects in China. From 10 projects in 2021, the number rose to over 90 in 2022 and more than 100 in 2023. In Q1 2024, an additional 83 projects with planned investments exceeding 600 billion yuan were recorded (equivalent to about two-thirds of the global industry scale, which is currently around 125 billion US dollars, or approximately 900 billion yuan), though only 10 have commenced construction or production.

Investment is concentrated in regions with ample renewable resources, strong policy support, and high demand potential from end users, such as Northwest, Northeast, and North China. Inner Mongolia alone accounted for 59% of China's green hydrogen project investment in 2023.

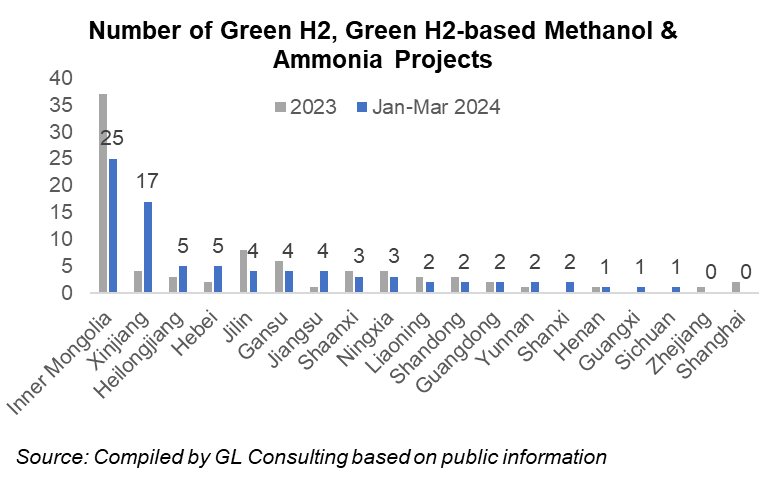

Higher Clean Marine Fuel Demand Boosts Green Methanol Projects Since 2023

Since H2 2023, new green hydrogen projects have primarily focused on producing green methanol. The EU CBAM has heightened the demand, leading to increased orders for green methanol-powered vessels. Development of green hydrogen-based ammonia has been slower compared to green methanol, due to the continued reliance on coal-based ammonia production in China.

From January to November 2023, China added 8.65 million tonnes/year of methanol production capacity using green hydrogen, nearly doubling the 4.85 million tonnes/year for hydrogen-based ammonia.

By the end of 2022, planned green hydrogen-based ammonia production capacity far exceeded that of green methanol, at 4.62 million tonnes/year and 500,000 tonnes/year, respectively.

Green Hydrogen Faces Significant Economic Challenges in Replacing Grey Hydrogen

Currently, due to their high production costs, green methanol and green ammonia do not have a price advantage over their market equivalents.

Given the current carbon emission trading prices and projected technological advancements, by 2030, only Inner Mongolia might achieve cost parity between green hydrogen and blue hydrogen. By 2060, nine provinces in northern and eastern China with abundant wind and solar resources could achieve cost parity between green and grey hydrogen.

If the carbon trading price rises to 500 yuan/tonne, 22 additional provinces could achieve green hydrogen substitution for grey hydrogen by 2060. Thus, enhancing the carbon trading market and gradually increasing carbon prices will be vital for green hydrogen development.

To get detailed full text, send an email to glconsulting@mysteel.com

Edited by Aggie Hu, huchenying@mysteel.com