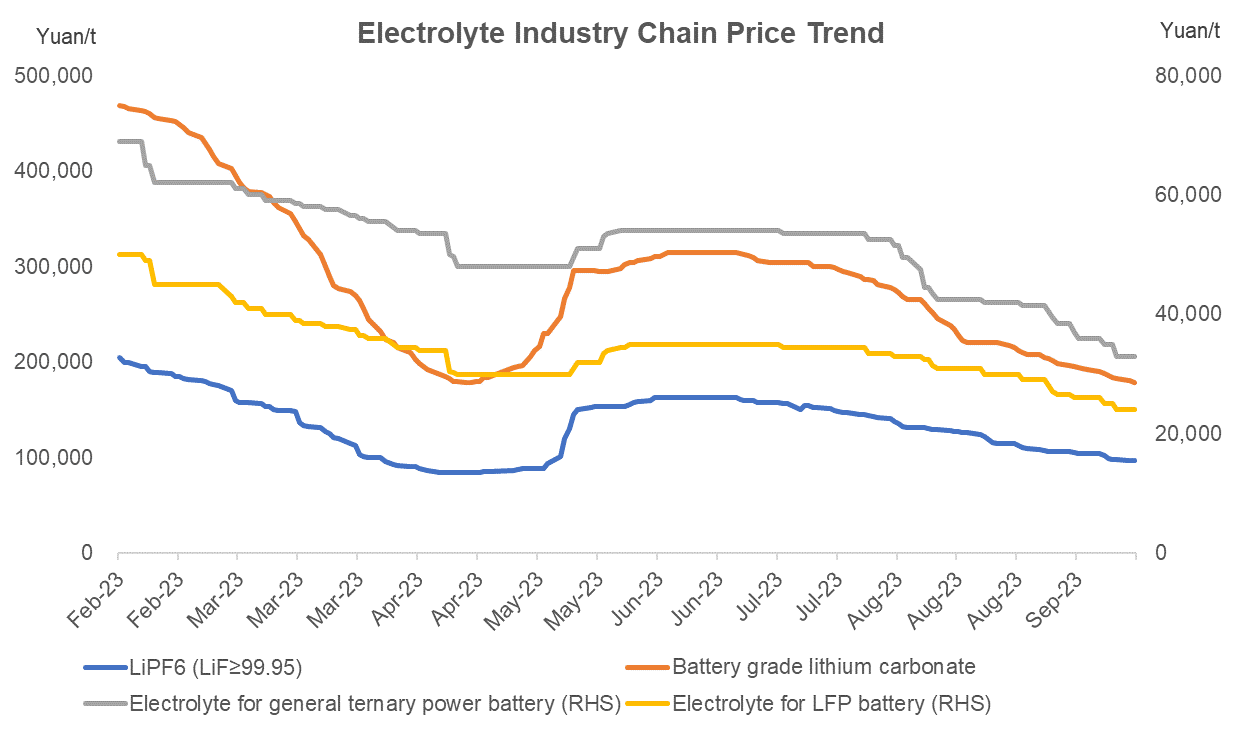

The electrolyte industry chain has been plagued by extensive price cuts recently with the traditional seasonal high failing to pay off.

Specially, LiPF6 prices dropped to Yuan 96,500/tonne as of September 26, down 16% month on month as a result of obvious oversupply and falling lithium carbonate prices.

Battery grade lithium carbonate prices posted the largest fall over September, which lost 19% on a monthly basis at Yuan 178,500/t as of September 26, followed by industrial grade lithium carbonate with a monthly decrease of 15%.

Source: Mysteel

A few LiPF6 traders surrendered some profits in order to destock and withdraw cash on the backdrop of shrinking cost, trailing by manufacturers which reduced the capacity utilization rates to avoid excessive stocks. Nevertheless, the transactions remained poor, weighing on LiPF6 prices.

Looking ahead, the electrolyte industry chain seems to be caught up in a bear market, featuring poor demand and palpably inventory pressure. Since the downstream and end-market players hold the upper hand, the LiPF6 prices are unlikely to gain momentum in the near term.

Written by Aggie Hu, huchenying@mysteel.com